News

Germany just created a real RFNBO demand signal

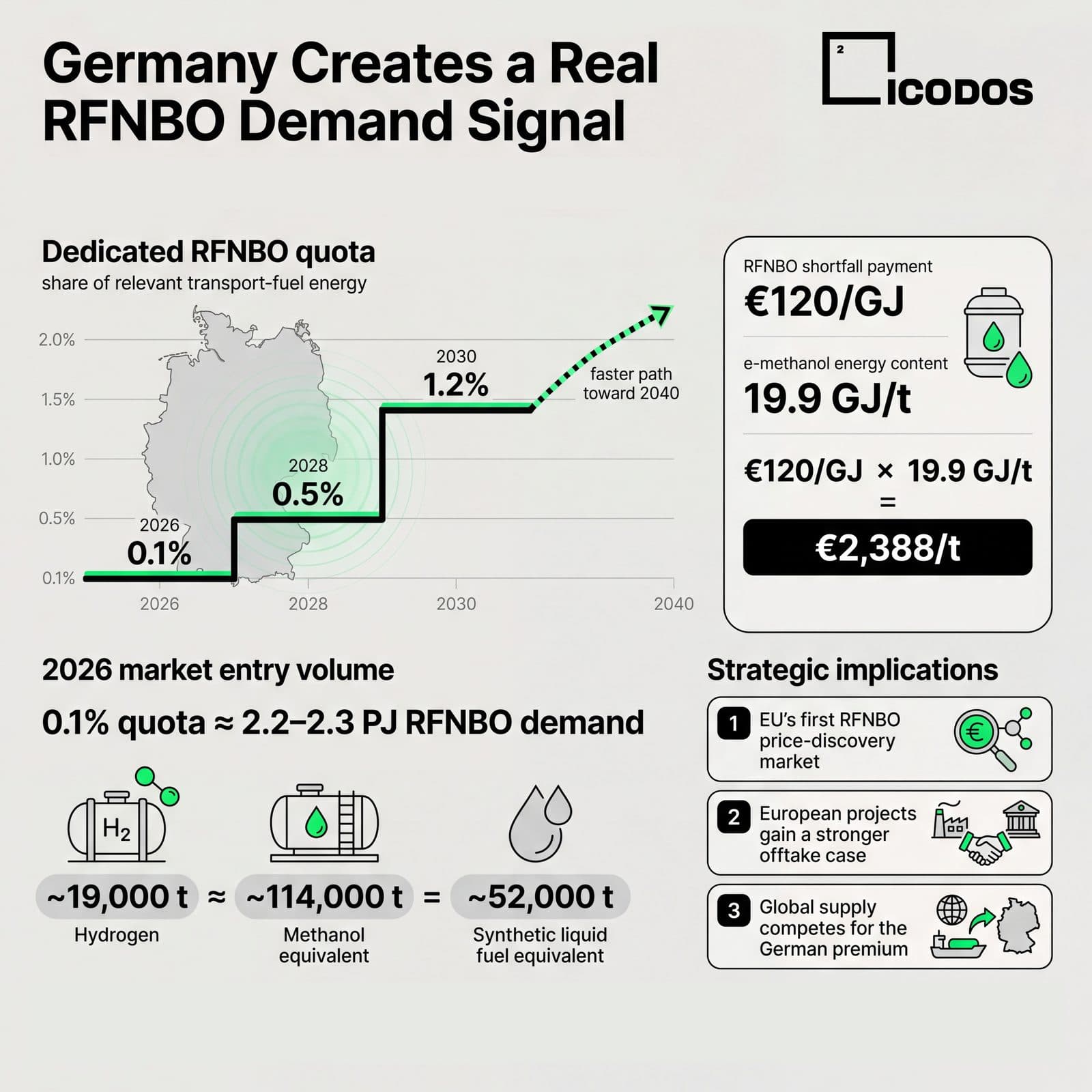

The Bundestag passed a dedicated RFNBO quota: 0.1% in 2026, 1.2% by 2030 — with a €120/GJ shortfall payment. For e-methanol that translates to a compliance-value ceiling of €2,388 per tonne. Why the market-formation effect matters more than the volume.

Germany just created a real RFNBO demand signal. The Bundestag has passed the reform of the greenhouse-gas reduction quota; Bundesrat approval is still pending, although the political path currently looks constructive. The important change is the dedicated quota for RFNBOs: green hydrogen and its derivatives, including synthetic fuels.

The trajectory and the number that matters

Based on the draft trajectory, the quota starts at 0.1% of relevant transport-fuel energy in 2026, rises to 0.5% in 2028 and reaches 1.2% in 2030 — with the Bundestag amendment pointing to a faster path toward 2040. The RFNBO shortfall payment is set at €120/GJ, and that number changes the procurement logic. For e-methanol, one tonne contains roughly 19.9 GJ of energy: €120/GJ × 19.9 GJ/t = €2,388/t. We read this as a compliance-value ceiling — before logistics, certification, credit trading, banking rules and competing compliance options.

Small volumes, large market-formation effect

The 2026 volume itself remains small: a 0.1% quota creates roughly 2.2–2.3 PJ of RFNBO energy demand in Germany — approximately 19,000 tonnes of hydrogen, 114,000 tonnes of methanol equivalent, or 52,000 tonnes of synthetic liquid fuel equivalent. These are early-market volumes. The strategic effect sits in market formation: fuel suppliers now have a reason to build RFNBO sourcing, registry, verification and offtake capabilities immediately; developers gain a clearer demand anchor; financiers gain a policy-backed compliance customer; traders gain a reason to test which certified molecules can actually clear into Germany.

Three likely implications

First, Germany becomes the EU's first RFNBO price-discovery market: the first tenders will reveal which products are bankable, which certification routes are trusted, and where obligated parties place value. Second, European projects gain a stronger offtake case: a penalty-backed quota helps close the familiar coordination loop between producers, buyers and financiers — especially for projects with credible renewable power, eligible CO₂ and EU-grade certification. Third, global supply will compete for the German premium: the market will reward eligibility, documentation and delivered cost.

The practical lens

Where direct electrification works, electrons usually carry the system-cost advantage. Where molecules are required, certified RFNBOs become valuable. Where one molecule can serve several demand pools, optionality becomes strategic. The scarcity is eligible molecules — and e-methanol, with existing logistics, shipping and chemicals relevance, and a clear link to CO₂ utilisation, is well positioned in that merit order.